Interactive

Figure 1

Demand should surpass pre-pandemic levels this year

Figure 2

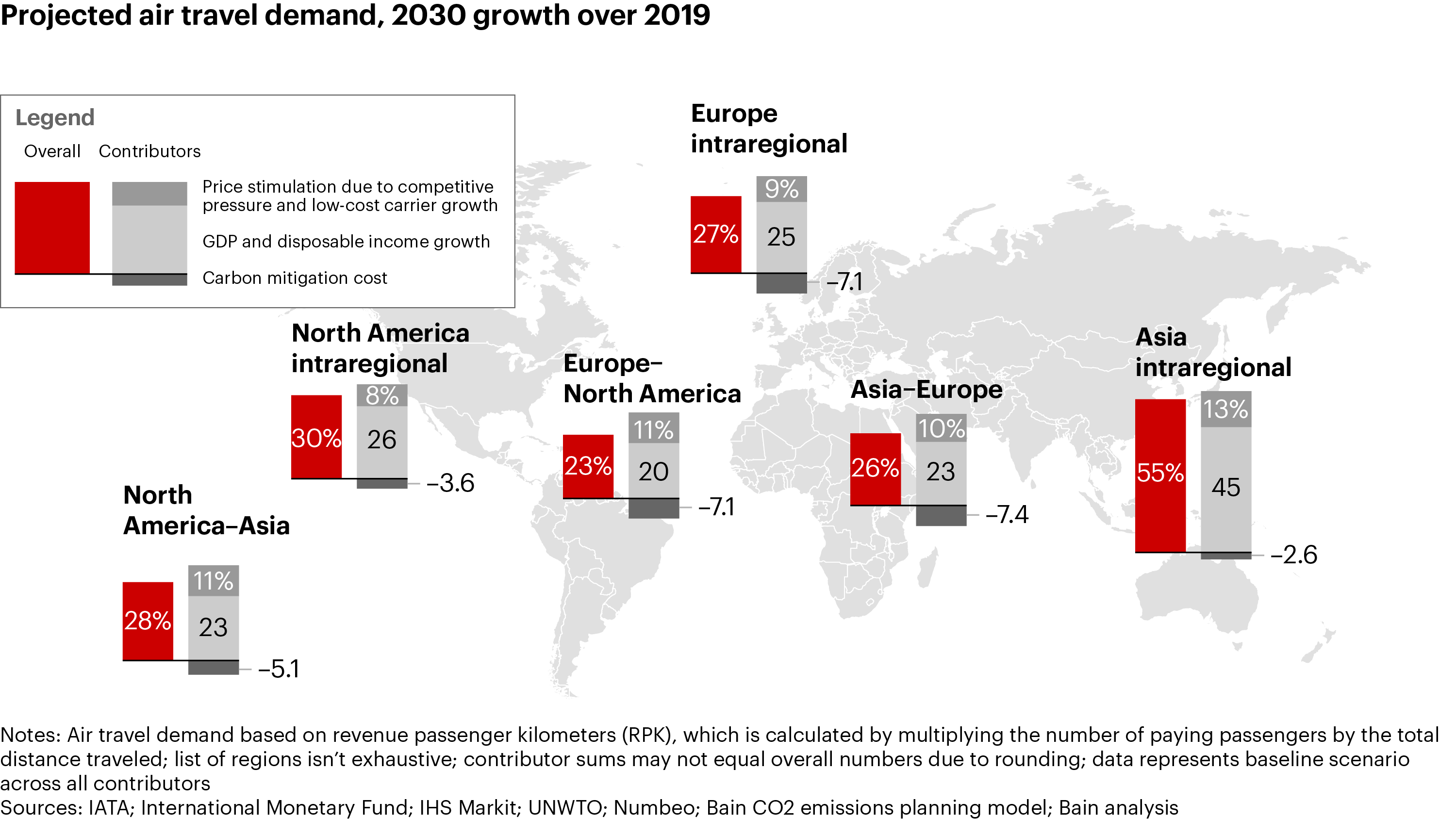

Asia will lead expansion as three growth factors hit regions differently

Figure 3

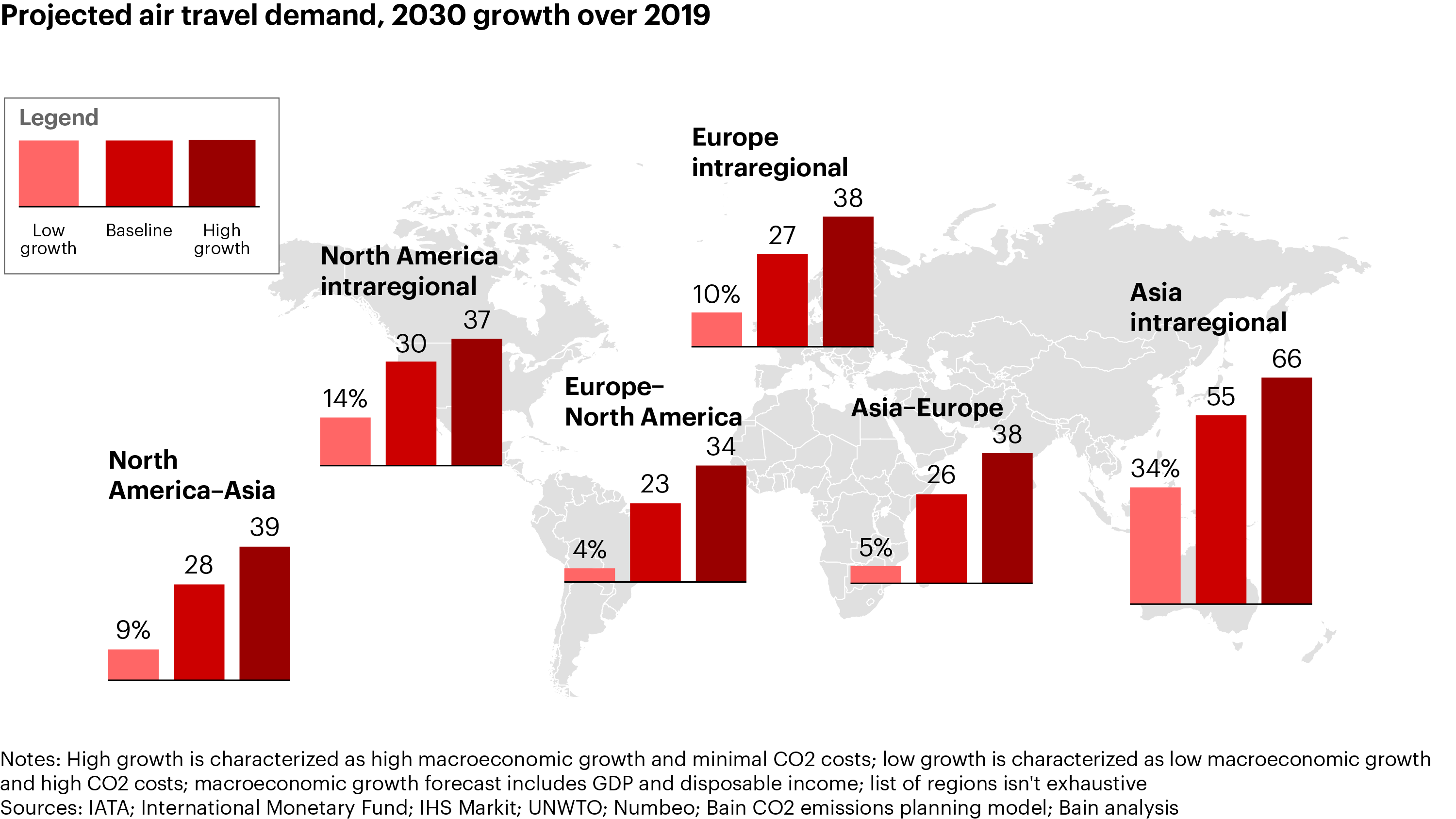

European long-haul flights are the most vulnerable to economic swings

Custom Air Travel Forecasts

Improve your financial, capacity, and commercial planning with granular air traffic demand projections.

Launched in May 2020, our air traffic forecast was originally designed as a response to pandemic uncertainties. It has since evolved to cover other key factors: macroeconomic growth, levels of disposable income, and carbon mitigation costs. Now extended to the end of the decade, the forecast is updated regularly using the latest information.

Here is the outlook as of the end of the second quarter of 2024:

- Annual air travel demand remains on track to surpass the 2019 total this year, as measured by revenue passenger kilometers (RPK)—the number of paying passengers multiplied by the total distance traveled. As expected, this year’s first-quarter demand exceeded pre-pandemic levels (see Figure 1 above). By 2030, we anticipate global RPK will reach 11.4 trillion in our base scenario, which would be 136% of 2019 volume. Meanwhile, several factors have contributed to changes in the forecasts for specific regions and countries (see Figures 2 and 3).

- A slightly improved macroeconomic forecast raised the 2030 demand outlook for North American intraregional travel by 3% vs. the previous quarter. This is equivalent to a $4 billion revenue increase at current yields.

- Europe’s intraregional demand outlook rose about 1%, the equivalent of slightly more than $1 billion in revenue. Most of the growth is expected to come from southern European countries Turkey, Spain, and Italy.

- We continue to anticipate significant intraregional demand growth in Asia—a 55% increase from 2019 to 2030. Still, projected demand fell about 5% from our previous update due to a slight dip in the region’s macroeconomic forecast and weaker-than-expected performance during the previous quarter, particularly for northeast Asia and China domestic flights.

- We estimate that the airline industry’s current decarbonization measures will result in a net 3.4% increase in its global CO2 emissions by 2030 vs. 2019 levels. This is based on the outlook that a 23% reduction in CO2 emissions per RPK (thanks to fleet renewal and sustainable aviation fuel usage) would be more than offset by a 36% increase in global RPK. It would require an additional carbon tax equivalent to 5% of average ticket prices worldwide in order for the industry to maintain its 2019 C02 emissions volume in 2030, according to our forecast.

Projected market and financial information, analyses, and conclusions are based (unless sourced otherwise) on external information and Bain & Company’s judgment. They are intended as a guide only and should not be construed as definitive forecasts or guarantees of future performance or results. No responsibility or liability whatsoever is accepted by any person, including Bain & Company, Inc., or its affiliates and their respective officers, employees, or agents, for any errors or omissions.

Bain's Quarterly Airlines Newsletter

Subscribe to receive our airlines insights in your inbox every quarter.